Virtual Power Plant Market Size to Surpass USD 39.31 Billion by 2034

Europe Leads; Asia Pacific Emerges as Fastest-Growing Region

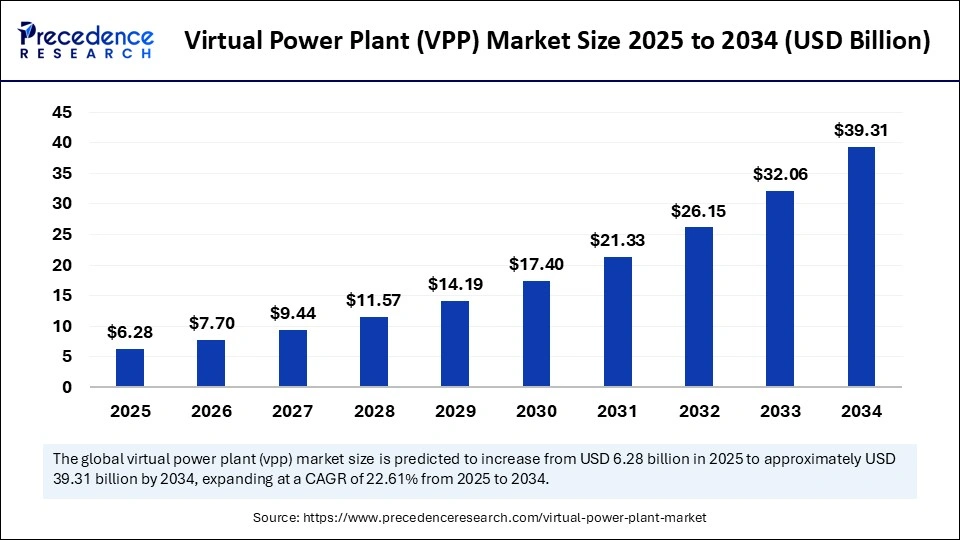

The Virtual Power Plant (VPP) market is projected to surge from $6.28 billion in 2025 to a staggering $39.31 billion by 2034, thanks to robust integration of renewables, digital intelligence, and regulatory support. With breakthroughs in AI and grid flexibility, Europe maintains its dominance, while Asia Pacific races ahead as the fastest-growing region, propelled by smart grid innovation and elevated energy demand.

The Virtual Power Plant market orchestrates diverse distributed energy resources (DERs) solar, wind, batteries, and even electric vehicles, into grid-responsive networks. Driving this transformation are soaring renewable penetration, smart platforms, and growing policy incentives. As the sector gallops at a 22.61% CAGR, utilities, commercial entities, and industrial giants are embracing VPPs for efficiency and resilience.

Virtual Power Plant Market Key Insights

-

The global VPP market will reach USD 39.31 billion by 2034, up from USD 6.28 billion in 2025.

-

Europe reigns as the top region, capturing over 41% market share in 2024.

-

Asia Pacific stands as the fastest-growing market, powered by rapid urbanization and smart grid investments.

-

Demand response emerged as the dominant technology segment, with 47.97% market share in 2024.

-

Solar PV systems led the power source segment, while battery energy storage is set for the fastest growth ahead.

-

The industrial segment captured 39.2% of 2024 market share, due to high, stable energy demands.

-

Tier 1 players control 40–50% of the market, with major innovators like Siemens, Next Kraftwerke, and Centrica highlighted.

Revenue Breakdown Table

| Year | Global Market Value (USD Billion) | Europe Market Value (USD Billion) | CAGR (2025–2034) |

|---|---|---|---|

| 2025 | 6.28 | 2.61 | 22.61% |

| 2026 | 7.70 | 3.20 | – |

| 2034 | 39.31 | 16.36 | 22.61% |

AI: Transforming Virtual Power Plants

Modern VPPs rely on artificial intelligence to analyze real-time data and maximize resource allocation—balancing supply, predicting demand, and managing distributed assets for optimal profitability and grid stability. AI-driven platforms power automated decision-making, which can rapidly engage demand response resources during spikes, and forecast the variability of solar and wind output to enhance overall grid health.

Additionally, AI is crucial for integrating electric vehicles into grids using V2G technology. This not only helps stabilize infrastructure but also turns EVs into grid assets able to discharge when needed—further decentralizing and democratizing grid management.

Virtual Power Plant Market Growth Factors

The VPP market’s fast rise is anchored in:

-

Expanding use of renewables and the necessity to manage intermittency.

-

Digitization, especially IoT and advanced analytics for resource aggregation.

-

Progress towards regulatory frameworks that support market entry and innovation.

Challenges and Cost Pressures

Despite market optimism, progress is constrained by fragmented regulations, high initial costs, and technical integration hurdles. Regulatory inconsistency remains a significant barrier, especially for new entrants seeking standardized market frameworks and predictable returns.

Are Decentralized Grids the Future of Power?

As global energy systems pivot towards decentralization, VPPs are set to become the backbone of flexible, resilient grids leveraging thousands of scattered, intelligent assets to create new revenue streams and reduce the need for costly conventional generation.

Can VPPs Unlock Opportunities Through Electric Vehicles?

With V2G (Vehicle-to-Grid) adoption rising, VPPs can tap into the immense storage potential of EVs, mitigating the intermittent nature of renewables and providing lucrative grid-balancing services during critical peaks.

What Drives Demand Response as the Leading Segment?

Demand response dominates due to its scalability, cost-effectiveness, and critical role in maintaining grid flexibility without new infrastructure, leveraging smart platforms, IoT, and AI for instant grid impact.

Regional and Segmentation Analysis

Europe

Europe advances on the back of strong renewable targets, advanced grid technology adoption, and supportive liberalized markets. Germany leads with policy innovation and green investment, setting benchmarks in flexibility and the hydrogen transition.

Asia Pacific

Asia Pacific’s rapid economic growth and government mandates fuel its position as the fastest-growing VPP region. Investments in smart grids and energy storage, especially in China and India, are expanding market frontiers.

North America

The region moves forward under FERC Order 2222, enabling aggregated DERs’ participation in wholesale markets and incentivizing VPP technology development with tax credits for solar and storage.

Also Read: Energy Cloud Platform Market Size to Soar USD 36.82 Billion by 2034

Top Companies in the Virtual Power Plant Market

Tier I – Major Players

These are dominant global players with a comprehensive portfolio across software, hardware, grid integration, and commercial-scale VPP deployments. Each holds a significant share individually and together they account for approximately 40–50% of the total market revenue.

- Siemens AG: Siemens is a leading player in the market through its DEOP (Decentralized Energy Optimization Platform), enabling real-time monitoring, control, and optimization of distributed energy resources across industrial, commercial, and grid-scale applications.

- Schneider Electric SE: Schneider Electric contributes via its EcoStruxure™ platform and through its subsidiary AutoGrid, offering advanced VPP software solutions for energy aggregation, demand response, and AI-driven grid optimization.

- Tesla, Inc.: Tesla operates large-scale VPPs using its Powerwall and Powerpack battery storage systems, integrating thousands of residential and commercial energy assets to deliver grid services, particularly in regions like Australia and California.

- General Electric Company (GE): GE supports the VPP market through GE Digital Energy and its DERMS (Distributed Energy Resource Management System) solutions, which help utilities manage and dispatch decentralized assets for grid flexibility and resilience.

Tier II – Mid-Level Contributors

These companies have a strong presence in regional markets or specific segments of the value chain (e.g., demand response, DER aggregation, energy trading). Collectively, they contribute around 30–35% of the market.

- ABB Ltd.: ABB offers advanced grid automation and control technologies that support the seamless integration and optimization of distributed energy resources, playing a key role in enabling scalable and secure VPP infrastructure globally.

- Next Kraftwerke GmbH: As one of Europe’s largest VPP operators, Next Kraftwerke aggregates thousands of decentralized energy units into a cloud-based power plant, enabling real-time energy trading and grid balancing services across multiple markets.

- AutoGrid Systems Inc.: AutoGrid provides AI-powered energy management and VPP software platforms that help utilities and energy providers aggregate and control DERs for demand response, flexibility markets, and predictive analytics.

- Enel X: Enel X operates one of the largest demand response and VPP networks globally, integrating DERs and flexible loads to provide real-time grid services, primarily through its smart energy management platform.

- AGL Energy: AGL Energy is a pioneer in deploying residential and commercial-scale VPPs in Australia, integrating rooftop solar, battery storage, and smart inverters to support grid stability and customer energy optimization.

Tier III – Niche and Regional Players

These are smaller firms or startups focused on local implementations, niche VPP solutions, or specialized technologies. Individually, their market share is modest, but together they contribute around 15–20% of the global revenue.

- Limejump Ltd. (UK)

- Flexitricity Ltd. (UK)

- Sunverge Energy Inc. (U.S.)

- Enbala Power Networks (now part of Generac)

- Blue Pillar

- Other regional utilities and tech startups

Segments Covered in the Report

By Technology

- Demand Response

- Direct Load Control

- Time-of-Use Management

- Distributed Energy Resources (DER) Management

- Solar PV Integration

- Wind Energy Integration

- Battery Energy Storage Systems (BESS)

- Mixed-Asset Configurations

- Hybrid DER Management

- Integrated Demand Response & Storage

- Grid Integration & Control Systems

- Smart Inverters

- SCADA Systems

- Predictive Analytics & AI

- Energy Forecasting

- Predictive Maintenance

By Component

- Software Platforms

- Energy Management Software

- Optimization & Dispatch Software

- Services

- Consulting & Integration

- Operation & Maintenance

- Hardware

- Sensors & Controllers

- Communication Devices

- Communication Infrastructure

- IoT Networks

- Cloud-based Platforms

By Power Source

- Solar Photovoltaic (PV) Systems

- Rooftop PV

- Utility-Scale PV

- Battery Energy Storage Systems (BESS)

- Lithium-Ion

- Flow Batteries

- Wind Energy

- Onshore

- Offshore

- Combined Heat and Power (CHP)

- Electric Vehicles (EVs)

By End User

- Industrial

- Commercial

- Residential

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/7023

You can place an order or ask any questions. Please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344

- Battery Swapping Market Size to Touch USD 24.74 Billion by 2035 - March 5, 2026

- Dental Air Polishing System Market Size to Reach USD 1603.54 Million by 2035 - March 4, 2026

- Cryoballoon Ablation System Market Size to Surpass USD 2.49 Billion by 2035, Propelled by 5.70% Growth in Minimally Invasive Cardiac Care - March 2, 2026