Thermal Management for Data Centers Market Size to Hit $33.72 Billion by 2034

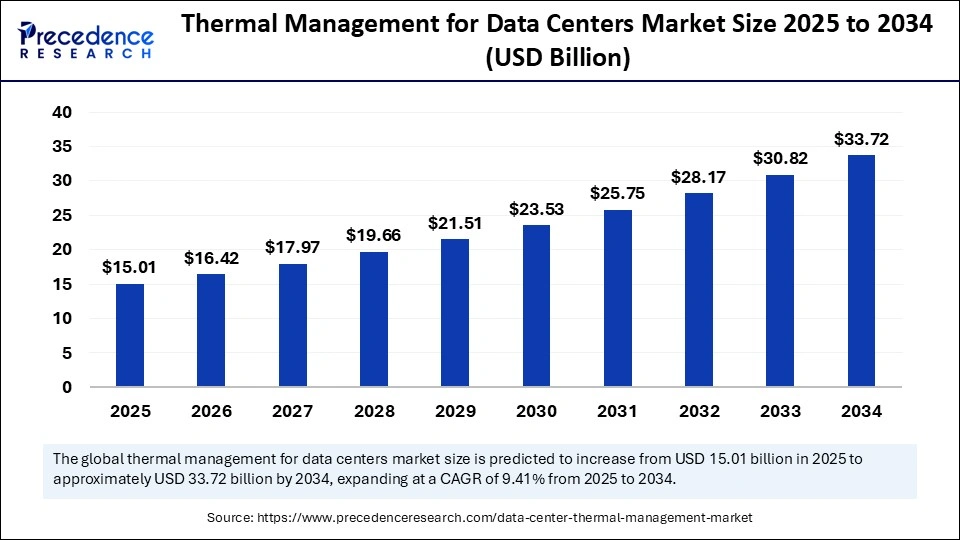

The global thermal management for data centers market is on a rapid growth trajectory, with a projected valuation of $33.72 billion by 2034, expanding at a robust CAGR of 9.41% from 2025 to 2034. This surge is fueled by the escalating demand for energy-efficient cooling solutions to manage the rising heat loads generated by hyperscale, cloud, and edge data centers. As digital transformation accelerates and AI-driven workloads intensify, the need for advanced thermal management technologies is becoming a critical operational priority for data center operators worldwide.

With the global data center market experiencing exponential growth, effective thermal management is no longer a luxury, it’s a necessity. The market’s expansion is driven by the need to maintain optimal performance, minimize downtime, and reduce energy consumption in environments where thousands of servers operate 24/7. The integration of AI and IoT-enabled devices is further enhancing thermal control, enabling real-time monitoring and predictive maintenance to optimize energy use and operational efficiency.

Thermal Management for Data Centers Market Key Insights

-

The global thermal management for data centers market was valued at $15.01 billion in 2025 and is expected to reach $33.72 billion by 2034.

-

North America dominated the market in 2024, capturing a 40% share, while Asia Pacific is projected to grow at the fastest CAGR.

-

Air-based cooling held a 40% market share in 2024, but liquid-based cooling is growing at the fastest rate.

-

Hyperscale data centers contributed the highest market share in 2024, while colocation/cloud data centers are expected to grow the fastest.

-

The IT & telecom sector led the market with a 45% share, while retail & e-commerce is projected to grow at a significant CAGR.

-

On-premise/in-house cooling systems held a 60% share in 2024, but modular/prefabricated cooling units are set for rapid growth.

AI’s Role in Thermal Management

Artificial intelligence is revolutionizing thermal management in data centers by enabling real-time, intelligent control of cooling systems. AI applications leverage predictive analytics, machine learning, and IoT sensors to monitor temperature, humidity, and airflow, dynamically adjusting cooling capacity, fan speed, and liquid flow based on workload and heat generation. This not only improves operational efficiency but also reduces power usage effectiveness (PUE), lowering energy costs and enhancing equipment reliability.

Vendors and startups are integrating AI across air, liquid, and hybrid cooling solutions, making data centers more efficient, scalable, and sustainable. The adoption of AI-driven monitoring and automation platforms is helping operators optimize cooling performance, minimize downtime, and support the growing demands of cloud, edge, and advanced digital workloads.

Thermal Management for Data Centers Market Growth Factors

The thermal management for data centers market is being driven by several key factors:

-

Exponential growth in global data traffic and digital transformation

-

Expansion of hyperscale and edge data centers

-

Rising power consumption and heat generation from cloud services and high-performance computing workloads

-

Integration of AI and IoT-enabled devices for real-time monitoring and predictive maintenance

-

Increasing focus on energy efficiency, sustainability, and green data center initiatives

Thermal Management for Data Centers Market Scope

| Report Coverage | Details |

| Market Size in 2025 | USD 15.01 Billion |

| Market Size in 2026 | USD 16.42 Billion |

| Market Size by 2034 | USD 33.72 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 9.41% |

| Dominating Region | North America |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2025 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Cooling Technology, Component, Data Center Type, End-User / Industry Vertical, Cooling Infrastructure Type, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Opportunity and Trend: What’s Driving the Market?

Why is liquid-based cooling growing faster than air-based cooling?

Liquid-based cooling offers superior thermal efficiency, enabling higher server density with lower energy consumption. Its sustainability benefits, including reduced carbon footprint and water usage, align with global green data center initiatives. Major vendors are investing in modular, scalable liquid cooling solutions that can be integrated into existing data center architectures.

What is driving the growth of colocation/cloud data centers?

The rising demand for scalable, cost-efficient IT infrastructure is driving the growth of colocation/cloud data centers. As more companies outsource IT systems to colocation and cloud services, rapid facility expansion has increased the need for thermal management solutions. Key priorities such as flexibility, uptime reliability, and sustainability have driven the adoption of modular air-based cooling, liquid cooling, and AI-driven temperature optimization.

How are retail & e-commerce companies contributing to market growth?

Increased digitalization and the rise of online shopping have surged data center demands for retailers and e-commerce giants. These companies are investing in modular, scalable, and energy-efficient data centers to maintain performance while reducing their carbon footprint. The adoption of AI-driven personalization, logistics automation, and omnichannel strategies further expands computing requirements, creating a need for advanced cooling solutions.

Regional Analysis

North America leads the global market, capturing a 40% share in 2024, driven by its extensive network of hyperscale data centers and early adoption of advanced cooling technologies. The U.S. is a major player, serving as the hub for hyperscale and leading cloud service providers, with rapid adoption of liquid cooling and AI-driven monitoring systems.

Asia Pacific is expected to experience the fastest growth, fueled by rapid digital transformation, expansion of cloud computing, 5G networks, and government-led initiatives promoting digital infrastructure. China, in particular, is a major growth driver, with leading technology players investing heavily in next-generation data centers that necessitate advanced cooling technologies.

Europe is witnessing steady growth, driven by a strong emphasis on energy conservation, environmental regulations, and the expansion of cloud and colocation facilities. The UK is emerging as a leading player, supported by its mature digital economy and high cloud adoption rates.

Thermal Management for Data Centers Market Segment Insights

Cooling Technology Insights

Air-Based Cooling Dominates the Market

The air-based cooling segment held a 40% share of the thermal management for data centers market in 2024. Its dominance stems from low costs, ease of implementation, and proven reliability in both traditional and enterprise data centers. Systems like direct air cooling, hot/cold aisle containment, and rear door heat exchangers efficiently manage airflow using CRAC and CRAH units. Additionally, advancements in energy-efficient fans, intelligent airflow management, and containment designs have improved performance while reducing energy consumption.

Liquid Cooling Emerging as the Fastest-Growing Segment

Liquid-based cooling is set to expand rapidly due to its superior efficiency in managing high thermal loads from AI, machine learning, and HPC systems. Technologies such as direct-to-chip and immersion cooling support higher server density with lower energy use. The segment benefits from sustainability advantages like reduced carbon emissions and water usage, aligning with global green data center goals.

Component Insights

Cooling Units & Chillers Lead the Market

Cooling units and chillers, including CRAC and CRAH systems, captured a 38% market share in 2024. These systems are crucial for temperature and humidity control in high-density computing environments. Enhanced by variable-speed compressors, advanced controls, and eco-friendly refrigerants, they deliver energy efficiency and operational reliability—especially in enterprise and colocation data centers.

Heat Exchangers / Heat Sinks on the Rise

Heat exchangers and sinks are gaining traction as data centers shift to liquid and hybrid cooling solutions. Liquid-to-liquid and air-to-liquid exchangers efficiently transfer heat while maintaining low energy consumption. Growing adoption of immersion and direct-to-chip systems has also increased demand for compact, high-performance exchangers made from thermally conductive materials.

Data Center Type Insights

Hyperscale Data Centers Lead the Market

Hyperscale facilities held a 40% market share in 2024, driven by the massive computing needs of AI, big data, and cloud applications. These centers require scalable thermal management technologies—like liquid and hybrid cooling—to ensure efficiency and uptime. Innovations in smart airflow and direct-to-chip cooling support energy and cost optimization.

Colocation and Cloud Centers Growing Rapidly

Colocation and cloud data centers are expanding fast due to rising demand for flexible, cost-effective IT infrastructure. As organizations shift toward outsourcing and hybrid cloud models, modular cooling systems and AI-based temperature management have become essential for ensuring uptime, efficiency, and sustainability.

End-User / Industry Vertical Insights

IT & Telecom Segment Leads the Market

The IT and telecom sector held a dominant 45% share in 2024. Growth in cloud computing, 5G deployment, and IoT networks has created huge data loads, requiring robust thermal management for uninterrupted operations. Leading providers like AWS and Google Cloud are investing in energy-efficient and green cooling solutions to meet performance and sustainability goals.

Retail & E-Commerce Segment Growing Fast

The retail and e-commerce segment is witnessing strong growth driven by digitalization and real-time analytics. Data centers supporting online shopping and AI-powered personalization demand high-performance cooling systems. Retailers are increasingly investing in modular and scalable data centers to handle fluctuating workloads while reducing energy consumption.

Cooling Infrastructure Type Insights

On-Premise Cooling Systems Hold 60% Share

In 2024, on-premise or in-house cooling systems accounted for 60% of the market, driven by their reliability, customization, and control advantages. Enterprise and hyperscale data centers prefer in-house systems for mission-critical workloads. AI-based monitoring is being integrated to improve efficiency and reduce downtime across traditional setups.

Modular Cooling Units Set for Strong Growth

Modular or prefabricated cooling systems are gaining popularity for their scalability, quick deployment, and cost efficiency. These systems, pre-engineered and factory-assembled, are ideal for colocation and edge facilities. Supporting both air and liquid cooling, modular systems help operators meet sustainability and energy targets while adapting to evolving data center demands.

Latest Breakthroughs and Key Companies

The market is witnessing significant breakthroughs from leading companies:

-

Vertiv: Announced the Vertiv AI Infrastructure Program in August 2025 to enhance data center efficiency and thermal performance. The company also introduced next-generation liquid cooling solutions for high-density AI and HPC data centers.

-

Schneider Electric: Partnered with NVIDIA to launch AI-ready data center solutions, including a 132 kW-per-rack liquid-cooled AI cluster reference design.

-

Rittal: Offers advanced IT cooling systems, enclosures, and modular data center infrastructure, with innovations in scalability, automation, and energy-efficient operation.

-

Asetek: Pioneer in liquid cooling technology, known for direct-to-chip and immersion cooling systems that enable significant power savings and improved heat dissipation.

-

Green Revolution Cooling (GRC): Leader in immersion cooling, offering ICEraQ systems that submerge IT hardware in dielectric fluid for ultra-efficient, silent, and sustainable heat management.

Other notable companies include STULZ, Airedale International, Johnson Controls, Mitsubishi Electric Hydronics & IT Cooling Systems, Chilldyne, LiquidCool Solutions, Air Enterprises, Climaveneta, Coolcentric, Dell, Nortek Air Solutions, NTT, Thermal Care, Danfoss, Vigilent, Pentair, and Data Aire.

Challenges and Cost Pressures

Despite the market’s growth, operators face several challenges and cost pressures:

-

High capital expenditure for advanced cooling solutions

-

Supply chain volatility and component shortages

-

Increasing regulatory and sustainability mandates

-

Rising electricity prices and the need for carbon-neutral operations

Thermal Management for Data Centers Market Segments Covered in the Report

By Cooling Technology

- Air-Based Cooling

- Direct Air Cooling

- Rear Door Heat Exchangers

- Hot/Cold Aisle Containment

- Liquid-Based Cooling

- Direct-to-Chip Cooling

- Immersion Cooling

- Rear Door Heat Exchangers (Liquid)

- Hybrid / Combined Cooling

- Air-Liquid Hybrid Systems

- Other Cooling Technologies

- Thermoelectric Cooling

- Phase-Change Cooling

By Component

- Cooling Units / Chillers

- Computer Room Air Conditioners (CRAC)

- Computer Room Air Handlers (CRAH)

- Chillers

- Cooling Infrastructure / Piping & Distribution

- Pipes & Valves

- Pumps & Distribution Units

- Heat Exchangers / Heat Sinks

- Liquid-to-Liquid Heat Exchangers

- Air-to-Liquid Heat Exchangers

- Fans & Airflow Management Devices

- Other Components

By Data Center Type

- Hyperscale Data Centers

- Enterprise Data Centers

- Colocation / Cloud Data Centers

- Edge Data Centers / Micro Data Centers

By End User / Industry Vertical

- IT & Telecom

- Cloud Service Providers

- Telecom Operators

- BFSI (Banking, Financial Services & Insurance)

- Government & Defense

- Healthcare & Life Sciences

- Manufacturing / Industrial

- Education & Research Institutes

- Retail & eCommerce

By Cooling Infrastructure Type

- On-Premise / In-House Cooling Systems

- Modular / Prefabricated Cooling Units

- Cloud / Managed Cooling Services

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/7091

You can place an order or ask any questions. Please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344

- ESG Software Market 2025: Comprehensive Key Players Ecosystem and Revenue Outlook - May 20, 2026

- ESG Software Market Worth Around USD 31.96 Billion by 2035 - May 20, 2026

- Hematopoietic Stem Cell Transplantation Market Size to Attain USD 24.32 Billion by 2035 as Precision Medicine and AI Reshape Blood Cancer Treatment - May 20, 2026