US Battery Logistics Market Size to Exceed USD 11.43 Billion by 2035 as EV Manufacturing and Energy Storage Expansion Accelerate Supply Chain Demand

Rising Electric Vehicle Production, Domestic Gigafactory Investments, and Advanced Logistics Technologies Propel Market Growth at 11.38% CAGR

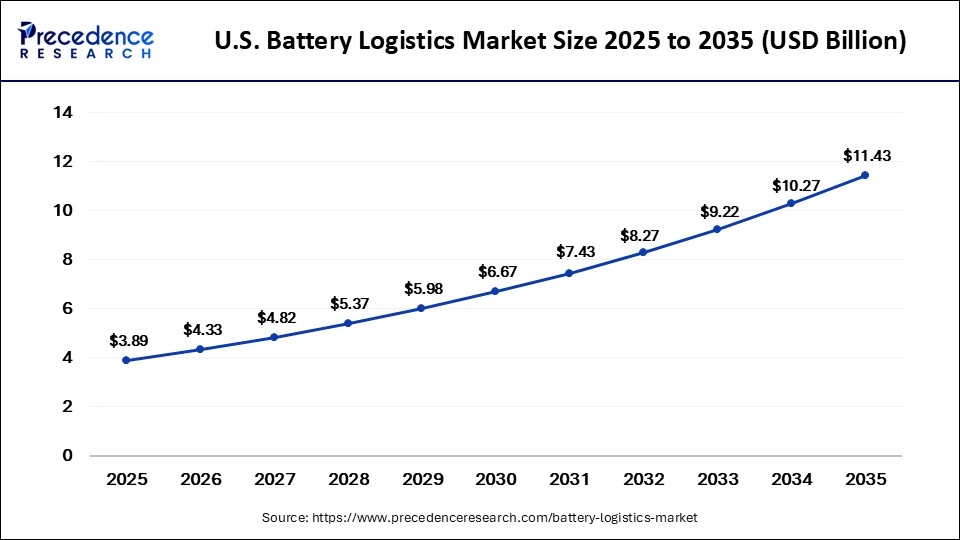

The U.S. battery logistics market is entering a transformative growth phase, fueled by the rapid expansion of electric vehicle (EV) manufacturing, rising investments in domestic battery production, and increasing deployment of energy storage systems. The market size was valued at USD 3.89 billion in 2025 and is projected to grow from USD 4.33 billion in 2026 to approximately USD 11.43 billion by 2035, registering a CAGR of 11.38% during the forecast period from 2026 to 2035.

Battery logistics has emerged as a critical pillar of the U.S. energy transition. From transportation and warehousing to packaging, inventory management, reverse logistics, and battery recycling, logistics providers are becoming essential partners for battery manufacturers, automotive OEMs, renewable energy developers, and electronics companies. As lithium-ion batteries continue to dominate the market and battery production scales nationwide, specialized logistics infrastructure is becoming increasingly important to ensure safety, compliance, traceability, and operational efficiency.

US Battery Logistics Market Key Insights

• The U.S. battery logistics market was valued at USD 3.89 billion in 2025 and is expected to reach USD 11.43 billion by 2035.

• The market is forecast to expand at a CAGR of 11.38% between 2026 and 2035.

• Lithium-ion batteries accounted for the largest market share in 2025 due to their widespread use in EVs, electronics, and energy storage systems.

• Transportation services emerged as the leading logistics service segment in 2025.

• Road transportation remained the dominant transportation mode because of its flexibility and nationwide accessibility.

• Electric vehicles represented the largest application segment in the market.

• Automotive OEMs generated the highest demand for battery logistics services in 2025.

• Flow batteries are projected to witness the fastest growth rate over the forecast period.

• Recycling and second-life battery logistics are expected to become major revenue-generating opportunities by 2035.

• California continues to lead the market, while Texas, North Carolina, and Massachusetts are rapidly expanding their battery logistics ecosystems.

U.S. Battery Logistics Market Revenue Outlook

| Year | Market Size (USD Billion) |

|---|---|

| 2025 | 3.89 |

| 2026 | 4.33 |

| 2035 | 11.43 |

| Market Metrics | Details |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| CAGR | 11.38% |

| Fastest Growing Battery Type | Flow Batteries |

| Dominant Battery Type | Lithium-Ion Batteries |

| Dominant Application | Electric Vehicles |

| Dominant End User | Automotive OEMs |

Why is Battery Logistics Becoming a Strategic Priority Across the United States?

The battery supply chain is becoming increasingly complex as the nation accelerates investments in electrification and clean energy infrastructure. Battery logistics providers are now responsible for managing highly sensitive materials that require strict safety procedures, temperature control, specialized packaging, and compliance with hazardous materials regulations.

As new gigafactories emerge across the country and battery production becomes more localized, logistics companies are being called upon to create resilient transportation networks capable of supporting battery manufacturing, distribution, storage, and recycling activities. This evolution is transforming logistics from a support function into a strategic component of the U.S. energy economy.

How is Artificial Intelligence Reshaping the U.S. Battery Logistics Market?

Artificial intelligence is revolutionizing battery logistics operations by improving visibility, predictability, and efficiency throughout the supply chain. AI-powered systems enable logistics operators to optimize delivery routes, predict demand fluctuations, monitor inventory levels, and improve warehouse utilization.

Advanced machine learning algorithms are also helping companies identify potential transportation risks and predict maintenance requirements before operational disruptions occur. This capability is especially valuable when handling lithium-ion batteries, which require strict safety standards and real-time monitoring.

The integration of AI with IoT sensors and digital tracking technologies is further strengthening supply chain transparency. Logistics providers can now track battery condition, location, and compliance status throughout transportation and storage processes, reducing risk while improving customer confidence.

A notable industry development occurred in March 2026 when Nuvocargo launched Nuvo AI, an AI-native freight execution platform designed to automate freight operations, optimize transportation routes, and enhance supply chain performance for North American shippers, including battery manufacturers and suppliers.

What Factors are Driving Growth in the U.S. Battery Logistics Market?

Explosive Growth in Electric Vehicle Manufacturing

The rapid increase in EV production remains the strongest catalyst for market growth. As automakers expand electric vehicle portfolios and establish domestic battery supply chains, demand for specialized logistics services continues to rise.

Battery packs, raw materials, and components must move efficiently between manufacturing plants, assembly facilities, distribution centers, and recycling operations. This creates substantial opportunities for logistics providers with expertise in battery handling and hazardous material transportation.

Expansion of Domestic Battery Gigafactories

Federal incentives and private investments are accelerating construction of battery gigafactories across the United States. These facilities require sophisticated logistics networks capable of supporting inbound raw material transportation and outbound battery distribution.

As production capacity expands, logistics providers are investing heavily in specialized infrastructure and digital supply chain technologies to meet growing demand.

Growth of Energy Storage Systems

The increasing deployment of utility-scale and commercial battery energy storage systems is generating additional logistics requirements. Large-scale battery projects require secure transportation, warehousing, installation support, and lifecycle management services.

The growing emphasis on renewable energy integration is expected to further strengthen demand for battery logistics solutions throughout the coming decade.

What Opportunities are Emerging for Logistics Providers in the Battery Recycling Economy?

One of the most promising opportunities lies within the rapidly expanding battery recycling ecosystem.

As millions of EV batteries approach end-of-life status over the next decade, demand for collection, transportation, storage, and recycling logistics services is expected to rise dramatically. Logistics companies capable of developing specialized reverse logistics capabilities will be well-positioned to capitalize on this emerging market.

The transition toward a circular battery economy is creating entirely new supply chains centered around battery recovery, material extraction, and second-life battery applications. These developments are expected to become major revenue generators for logistics providers through 2035.

How is Government Support Accelerating Market Expansion?

The U.S. government continues to play a crucial role in strengthening domestic battery supply chains through policy initiatives, funding programs, and manufacturing incentives.

Programs established under the Infrastructure Investment and Jobs Act (IIJA) and the Inflation Reduction Act (IRA) have stimulated large-scale investments in battery manufacturing, recycling facilities, and critical mineral processing projects. These initiatives are creating substantial demand for transportation, storage, and distribution services nationwide.

In March 2026, the U.S. Department of Energy announced a funding opportunity worth up to USD 500 million to expand domestic critical mineral processing, battery manufacturing, and battery recycling capabilities. The initiative is expected to strengthen logistics infrastructure and improve supply chain resilience across the battery value chain.

US Battery Logistics Market Segmentation Analysis

Battery Type Insights

Lithium-ion Batteries Dominated the Market in 2025

The lithium-ion batteries segment held the largest share of the U.S. battery logistics market in 2025. Strong demand from electric vehicles, consumer electronics, and energy storage systems, along with expanding domestic battery manufacturing and supportive government policies, drove the segment’s growth.

Flow Batteries to Grow at the Fastest Rate

The flow batteries segment is projected to register the highest CAGR during the forecast period. Rising investments in grid-scale energy storage and renewable energy integration are expected to increase demand for transporting and storing flow battery components.

Logistics Service Insights

Transportation Services Led the Market in 2025

Transportation services accounted for the largest market share in 2025 due to the large-scale movement of battery materials, components, and finished batteries. Growing battery production, hazardous material handling requirements, and expanding domestic and international trade supported segment growth.

Warehousing & Storage to Expand Rapidly

The warehousing & storage segment is expected to witness the fastest growth. Increasing demand for specialized battery storage facilities, smart warehouse technologies, and investments in battery gigafactories and recycling plants are driving the segment.

Transportation Mode Insights

Road Transportation Held the Largest Share

Road transportation dominated the market in 2025 because of its flexibility, extensive highway network, and efficient door-to-door delivery capabilities. The rapid expansion of EV manufacturing and battery production has further strengthened demand for road logistics.

Multimodal Transport to Record Strong Growth

The multimodal transport segment is anticipated to grow at the fastest pace. Companies are increasingly combining road, rail, air, and sea transportation to improve supply chain efficiency, lower logistics costs, and support cross-border battery trade.

Application Insights

Electric Vehicles (EVs) Dominated the Market

The EV segment captured the largest market share in 2025, supported by rising EV production, expanding battery manufacturing, government incentives, and the development of new vehicle assembly facilities across the U.S.

Energy Storage Systems to Grow the Fastest

The energy storage systems segment is expected to witness the highest growth during the forecast period. Increasing deployment of battery storage for renewable energy integration and grid modernization is driving demand for specialized battery logistics services.

Battery Lifecycle Insights

Finished Battery Distribution Led the Market

Finished battery distribution accounted for the largest market share in 2025 as battery manufacturers increased shipments to automakers, energy storage providers, and distributors. Rising domestic battery production further supported segment growth.

Recycling & Second-Life Logistics to Expand Rapidly

The recycling & second-life logistics segment is expected to grow at the fastest rate. Growing adoption of circular economy practices, expanding battery recycling infrastructure, and increasing volumes of end-of-life EV batteries are fueling market demand.

End User Insights

Automotive OEMs Held the Largest Market Share

Automotive OEMs dominated the market in 2025 due to the rapid growth of EV manufacturing. Strong partnerships between automakers and battery manufacturers, along with localized battery supply chains, significantly increased logistics demand.

Energy & Utility Companies to Register the Highest Growth

The energy & utility segment is expected to grow at the fastest CAGR. Rising investments in battery energy storage systems and renewable energy projects are creating strong demand for specialized battery logistics solutions.

State-Level Analysis

California

California remained a leading market due to its advanced EV ecosystem, strong battery manufacturing base, major ports, and supportive clean energy policies. Aggressive zero-emission vehicle targets continue to drive battery logistics demand.

Massachusetts

Massachusetts is emerging as a key market, supported by investments in battery research, renewable energy, and energy storage technologies. State incentives and research collaborations are expected to accelerate market growth.

Texas

Texas is witnessing significant growth because of expanding battery manufacturing, increasing renewable energy capacity, and major investments in EV infrastructure. Its strong transportation network and business-friendly environment further strengthen the market.

North Carolina

North Carolina is becoming an important battery logistics hub with rising investments in battery production and EV supply chain facilities. Favorable government policies, skilled labor, and new manufacturing projects are expected to support long-term growth.

US Battery Logistics Market Key Companies

- DHL Supply Chain: DHL Supply Chain offers battery logistics in the US across transport, storage, reverse logistics, recycling support, and end-to-end handling for EV batteries and other battery types.

- FedEx Corporation: FedEx Corporation supports battery shipping in the US through lithium-battery shipping guidance and hazardous-material shipping rules, with an emphasis on compliant packing and transport rather than a dedicated battery-logistics platform.

- UPS Supply Chain Solutions: UPS Supply Chain Solutions provides battery shipping support through supply-chain services, hazardous-material guidance, and approved shipping processes for batteries, including lithium batteries.

- Kuehne+Nagel: Kuehne+Nagel offers battery logistics for EV supply chains in the US, with services centered on compliant transport, warehousing, and multimodal freight support.

- DB Schenker: DB Schenker provides battery logistics covering pickup, transport, storage, reverse logistics, recycling, and multimodal movement across land, air, ocean, and rail.

- DSV A/S: DSV A/S did not have a clearly identified dedicated US battery-logistics offering in the sources reviewed, but it likely supports battery flows through broader freight forwarding and contract logistics capabilities.

- CEVA Logistics: CEVA Logistics offers battery solutions for lithium-ion and EV batteries, including IATA-certified shipping, storage, reverse logistics, dismantling, reconditioning, and recycling-oriented services.

- GEODIS: GEODIS positions itself around automotive and mobility logistics in the US, including smart eMobility battery solutions for transport and future mobility supply chains.

- Ryder System Inc.: Ryder System Inc. supports EV and clean-energy logistics through broader transportation, warehousing, and fleet services, but no dedicated US battery-logistics product was clearly identified in the reviewed sources.

- Expeditors International: Expeditors International shows battery-recycling and logistics capability through thought-leadership content, but no dedicated US battery-logistics service page was identified in the reviewed material.

- C.H. Robinson: C.H. Robinson supports renewable-energy and battery logistics in the US with multimodal transport, customs support, offload handling, and project logistics capabilities.

- XPO Logistics: XPO Logistics offers electric battery logistics with transport, storage, and hazardous-material handling, especially for lithium batteries.

- J.B. Hunt Transport Services: J.B. Hunt Transport Services did not have a clearly identified dedicated US battery-logistics offering in the sources reviewed, though it may still support battery shipments through general freight services.

- Nippon Express Holdings: Nippon Express Holdings did not have a clearly identified dedicated US battery-logistics offering in the sources reviewed, and its support for battery flows was not explicitly confirmed.

- Lineage Logistics: Lineage Logistics did not have a clearly identified dedicated US battery-logistics offering in the sources reviewed, so no battery-specific service could be confirmed from the retrieved material.

Segments Covered in the Report

By Battery Type

- Lithium-Ion Batteries

- Lead-Acid Batteries

- Nickel-Based Batteries

- Flow Batteries

- Others

By Logistics Service

- Transportation Services

- Warehousing & Storage

- Inventory Management

- Freight Forwarding

- Reverse Logistics & Recycling

By Transportation Mode

- Road Transportation

- Rail Transportation

- Ocean Freight

- Air Freight

- Multimodal Transport

By Application

- Electric Vehicles (EVs)

- Consumer Electronics

- Energy Storage Systems

- Industrial Equipment

- Others

By Battery Lifecycle

- Finished Battery Distribution

- Cell & Pack Logistics

- Raw Material Logistics

- End-of-Life Collection

- Recycling & Second-Life Logistics

By End User

- Automotive OEMs

- Battery Manufacturers

- Energy & Utility Companies

- Electronics Manufacturers

- Others

Read Also: Ceftriaxone Sodium Market Size to Attain USD 4.52 Billion by 2035

Get this report to explore global market size, share, CAGR, and trends, featuring detailed segmental analysis and an insightful competitive landscape overview @ https://www.precedenceresearch.com/sample/8521

You can place an order or ask any questions. Please feel free to contact us at sales@precedenceresearch.com |+1 804 441 9344

- US Battery Logistics Market Size to Exceed USD 11.43 Billion by 2035 as EV Manufacturing and Energy Storage Expansion Accelerate Supply Chain Demand - June 25, 2026

- Ceftriaxone Sodium Market Size to Attain USD 4.52 Billion by 2035 Amid Rising Burden of Severe Bacterial Infections - June 19, 2026

- Enterprise Collaboration Market Size to Reach USD 178.22 Billion by 2035 as Hybrid Work Culture Accelerates Digital Workplace Transformation - June 18, 2026