Inorganic Scintillators Market Set to Reach USD 1,520.10 Million by 2035

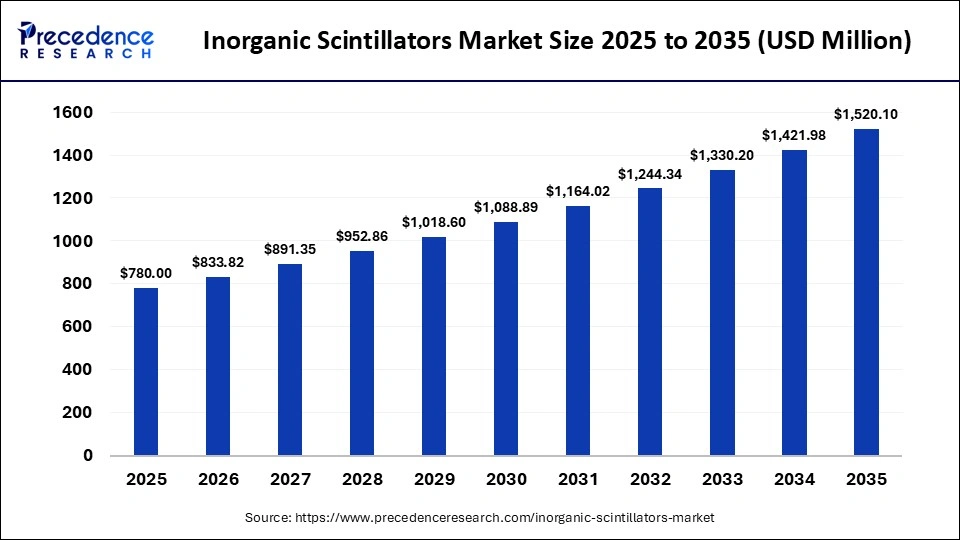

The global inorganic scintillators market is experiencing steady growth as demand for advanced radiation detection and high-resolution imaging technologies rises across healthcare, nuclear energy, and defense sectors. The market was valued at USD 780.00 million in 2025 and is projected to grow from USD 833.82 million in 2026 to USD 1,520.10 million by 2035, expanding at a CAGR of 6.90% during the forecast period.

This growth is largely driven by increasing adoption of medical imaging technologies such as PET, CT, and SPECT, along with rising concerns around nuclear safety and homeland security. Continuous advancements in scintillator materials are also improving detection sensitivity, accuracy, and performance across applications.

Read Also: Sovereign AI Infrastructure Market

Quick Insights: What Defines the Market Today?

The inorganic scintillators market is shaped by rising adoption in diagnostic imaging and radiation detection systems across industries. North America leads the global landscape, accounting for the highest share, while Asia Pacific is emerging as the fastest-growing region due to expanding healthcare and nuclear infrastructure. Sodium iodide (NaI) remains the most widely used material owing to its cost-effectiveness and high light yield. Medical imaging dominates application areas, supported by increasing chronic disease prevalence and demand for early diagnosis. Healthcare and diagnostics represent the largest end-use segment, reflecting the growing importance of precision imaging technologies in modern medicine.

How is AI Influencing the Inorganic Scintillators Market?

Artificial intelligence is playing a transformative role in enhancing the performance and efficiency of scintillator-based systems. AI-powered imaging algorithms are improving image reconstruction, enabling faster and more accurate diagnostics in applications such as CT and PET scans. This is particularly important in oncology and cardiology, where precision imaging is critical.

Moreover, AI is being integrated into radiation detection systems to enable real-time data analysis, anomaly detection, and predictive maintenance. These advancements are helping industries such as nuclear energy and homeland security improve operational efficiency while reducing risks associated with radiation exposure.

What are the Key Growth Drivers of the Market?

One of the primary drivers of the market is the increasing demand for advanced medical imaging technologies. The rising prevalence of chronic diseases and the growing need for early and accurate diagnosis are accelerating the adoption of scintillator-based imaging systems.

Additionally, the growing importance of radiation detection in nuclear power plants, defense, and homeland security is significantly boosting market demand. Governments and organizations are investing in advanced detection technologies to enhance safety, monitor radiation levels, and prevent potential threats.

What Opportunities and Trends are Shaping the Market?

Are Advanced Materials Driving the Next Wave of Innovation?

Yes, the development of high-performance scintillator materials such as lutetium-based crystals (LSO/LYSO) is enabling improved detection efficiency and faster response times, opening new opportunities in high-end imaging systems.

Is Healthcare Becoming the Largest Growth Engine?

Absolutely. With increasing adoption of PET, CT, and hybrid imaging systems, healthcare is emerging as the dominant sector driving demand for inorganic scintillators.

Will Silicon Photomultipliers (SiPM) Replace Traditional Technologies?

SiPM-based systems are gaining traction due to their compact size, higher efficiency, and ability to detect low-light signals, making them a key trend shaping the future of detection technologies.

Regional Analysis: Where is Growth Concentrated?

North America dominates the inorganic scintillators market, supported by advanced healthcare infrastructure, strong nuclear energy capabilities, and the presence of leading technology providers.

Asia Pacific is expected to grow at the fastest rate, driven by expanding healthcare systems, increasing investments in nuclear energy, and rising industrial applications. Europe also holds a significant share, supported by strong research initiatives and regulatory frameworks.

Segmental Analysis: How is the Market Structured?

Material Type Insights

Sodium iodide (NaI) leads the market with around 35% share due to its high efficiency and cost-effectiveness. Lutetium-based scintillators (LSO/LYSO) are expected to witness the fastest growth owing to their superior performance in advanced imaging systems.

Application Insights

Medical imaging dominates the market, accounting for approximately 40% share in 2025, followed by nuclear power and radiation detection. The increasing use of scintillators in PET, CT, and SPECT systems is driving this segment’s growth.

End-Use Insights

Healthcare and diagnostics lead the market with a 45% share, reflecting widespread use in imaging technologies. Energy & nuclear and defense sectors also contribute significantly to demand.

Detection Technology Insights

Photomultiplier tube (PMT)-based systems dominate with a 55% share due to their reliability and sensitivity, while SiPM-based systems are expected to grow rapidly due to technological advancements.

Competitive Landscape: Leading Companies

The market is moderately fragmented, with key players focusing on innovation, product development, and strategic collaborations.

Major companies include:

- Saint-Gobain Crystals

- Hamamatsu Photonics K.K.

- Hitachi Metals, Ltd.

- Amcrys-H Ltd.

- Rexon Components, Inc.

- Scionix Holland B.V.

- EPIC Crystal Company Limited

- Shanghai SICCAS High Technology Corporation

- Alpha Spectra, Inc.

- Dynasil Corporation of America

- Radiation Monitoring Devices, Inc.

- Korth Kristalle GmbH

- Zecotek Photonics Inc.

- Crytur, spol. s r.o.

- Detec Europe Ltd.

Recent Developments and Innovations

Recent advancements in scintillator materials are focused on improving radiation tolerance, response time, and cost efficiency. Innovations in lutetium-based and hybrid scintillators are enhancing performance in both medical imaging and high-energy physics applications. Additionally, integration with advanced detection technologies is enabling higher precision and efficiency.

Challenges and Cost Pressures

Despite steady growth, the market faces challenges such as high production costs of advanced scintillator materials and complex manufacturing processes. Additionally, maintaining performance under extreme conditions in nuclear and industrial environments adds to operational challenges.

Regulatory requirements related to radiation safety and environmental compliance also increase the cost burden for manufacturers and end-users.