Viral Vectors and Plasmid DNA Manufacturing Market Surges Toward $29.82 Billion by 2035

What is the Viral Vectors and Plasmid DNA Manufacturing Market Size in 2026?

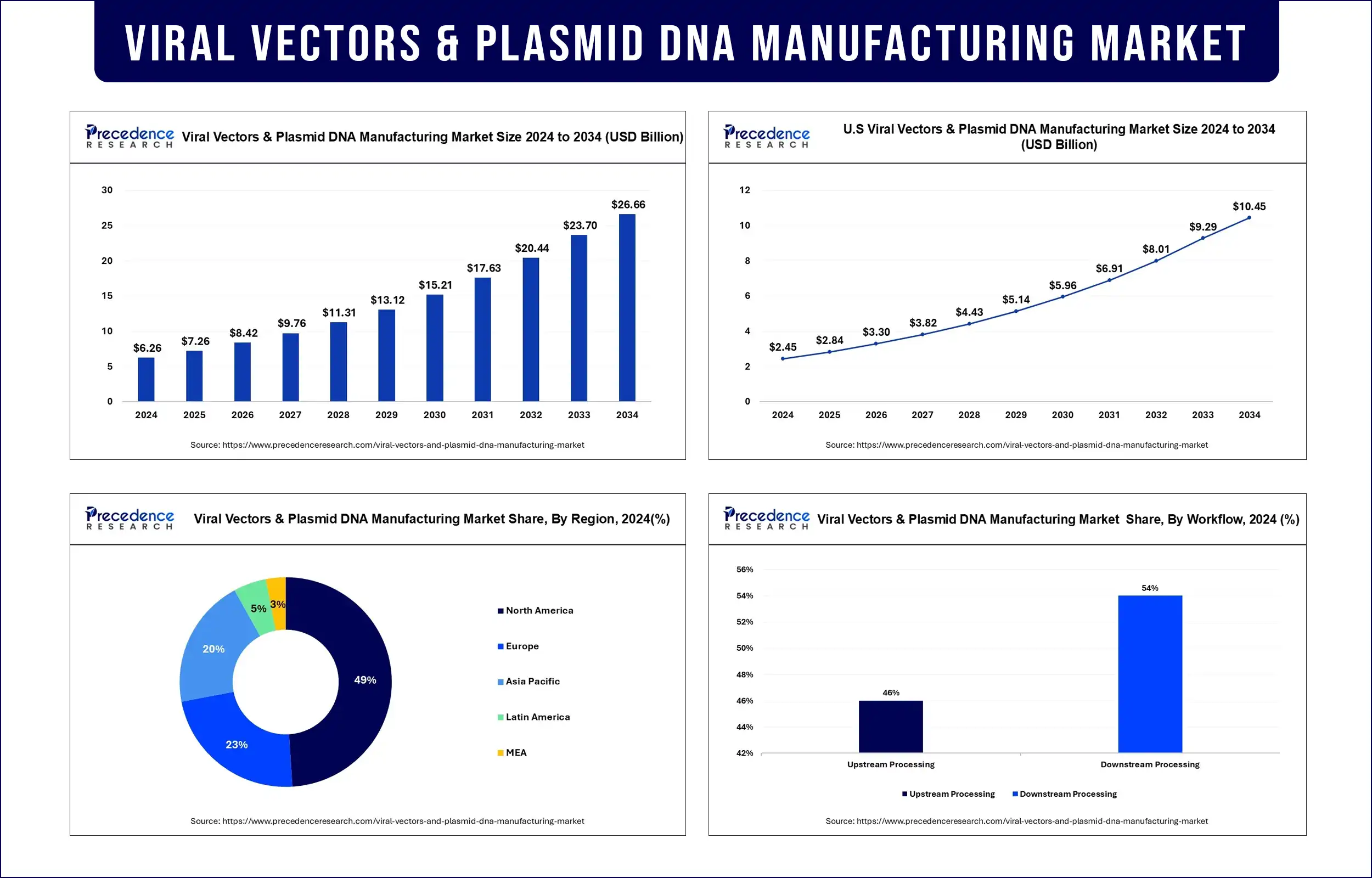

The global viral vectors and plasmid DNA manufacturing market is witnessing a transformative surge, projected to grow from approximately USD 6.68 billion in 2025 to USD 19.52 billion by 2033, expanding at a robust CAGR of 14.5%.

This rapid expansion is being driven by the accelerating pace of gene therapy innovation, CAR-T advancements, and mRNA-based vaccine platforms, all of which rely heavily on high-quality viral vectors and plasmid DNA for development and commercialization.

What Are the Key Highlights of the Viral Vector Manufacturing Market?

The market reached USD 6.68 billion in 2025 and is forecasted to hit USD 19.52 billion by 2033, reflecting strong double-digit growth.

North America dominated the global market with nearly 49% share due to advanced R&D infrastructure.

Asia-Pacific is emerging as the fastest-growing region, supported by expanding biotech investments.

The AAV (Adeno-Associated Virus) segment leads due to its precision in gene delivery.

Vaccinology accounted for the highest application share (22.08%), driven by demand for advanced vaccines.

Research institutes remain the largest end-users, reflecting strong academic and translational research activity.

How Is Artificial Intelligence Transforming This Market?

Artificial intelligence is increasingly becoming a cornerstone in viral vector and plasmid DNA manufacturing. AI-driven platforms are being used to optimize vector design, predict gene expression outcomes, and enhance production yields, significantly reducing trial-and-error cycles in bioprocessing.

Moreover, AI-enabled analytics are improving quality control and regulatory compliance by detecting impurities, predicting batch failures, and ensuring consistency in GMP manufacturing. As manufacturing complexity grows, AI is expected to bridge scalability gaps and accelerate commercialization timelines.

What Are the Major Growth Drivers Powering the Market?

The market is experiencing strong momentum due to a convergence of scientific, clinical, and industrial factors:

Rapid expansion of gene and cell therapy pipelines, especially in oncology and rare diseases

Increasing number of clinical trials and regulatory approvals for advanced therapies

Rising adoption of outsourcing to CDMOs due to high capital and technical barriers

Technological advancements such as suspension cell culture and transient transfection systems

Strong government and private investments in life sciences infrastructure

Market Scope

| Report Highlights | Details |

| Market Size by 2035 | USD 29.82 billion |

| Market Size in 2026 | USD 8.42 billion |

| Growth Rate | CAGR of 15.17% From 2026 to 2035 |

| Largest Market | North America |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | Vector Type, Application, Workflow, End-User, Disease |

| Regional Scope | Asia Pacific, North America, Europe, Latin America, the Middle East, and Africa |

What Trends Are Shaping the Future of the Market?

Is Gene Therapy Becoming the Core Demand Driver?

Yes, gene therapy is at the heart of this market’s growth. The increasing success of CAR-T therapies and AAV-based treatments has created unprecedented demand for scalable vector manufacturing solutions.

Are CDMOs Redefining Manufacturing Strategies?

Absolutely. Contract development and manufacturing organizations are enabling biotech firms to bypass infrastructure challenges, accelerating innovation while reducing costs.

Is Technology Innovation Solving Scalability Issues?

To a large extent. Innovations such as single-use systems, automated bioreactors, and integrated upstream-downstream workflows are improving efficiency and reducing production bottlenecks.

Market Outlook

Industry Overview

The viral vector and plasmid DNA manufacturing industry sits at the intersection of scientific innovation and industrial precision, transforming DNA from a biological blueprint into a powerful therapeutic asset. It underpins a rapidly expanding range of advanced treatments, including gene therapies, cancer immunotherapies, and solutions for rare genetic disorders.

Growth in this sector is driven by three core pillars:

Biotechnological innovation, enabling more efficient and targeted gene delivery

Robust manufacturing infrastructure, supporting scale and consistency

Stringent regulatory frameworks, ensuring safety and efficacy

Strategic collaborations between large pharmaceutical companies and agile biotech firms have become central to progress, combining scale with innovation. These partnerships are accelerating the transition from experimental therapies to commercialized treatments.

Sustainability Trends

Sustainability in viral vector and plasmid DNA manufacturing is evolving from a peripheral concern into a core operational philosophy. The industry is increasingly embracing eco-conscious bioprocessing, where environmental responsibility aligns with technological advancement.

Key developments include:

Adoption of energy-efficient manufacturing systems

Integration of water recycling and waste reduction processes

Use of bio-based and recyclable materials

Deployment of digital monitoring systems to optimize resource use

Although single-use technologies remain prevalent, efforts are underway to improve their recyclability and reduce environmental impact. The broader shift toward a circular bioeconomy reflects a growing recognition that scientific progress must be balanced with environmental stewardship.

Investment Landscape

The sector has entered a phase of strategic capital deployment, moving beyond speculative investment into long-term infrastructure building.

Major investment trends include:

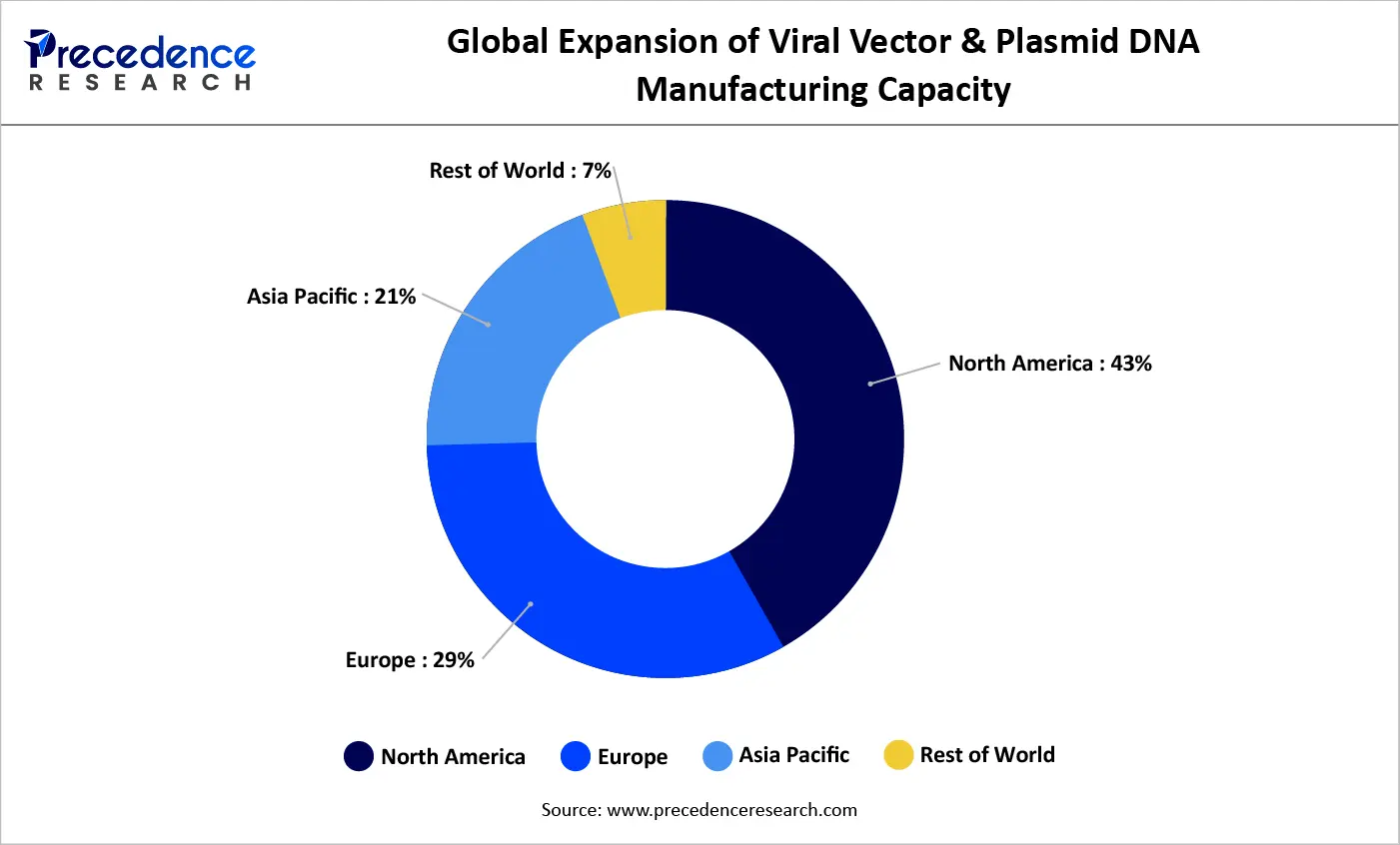

Expansion of automated, digitalized manufacturing facilities

Increased funding from venture capital, sovereign funds, and pharma giants

Government support through grants, subsidies, and tax incentives

Rising mergers and acquisitions, consolidating expertise and capabilities

These investments are not only scaling production capacity but also accelerating the broader genomic medicine revolution, making advanced therapies more accessible and commercially viable.

Sustainable Ecosystems and Startups

A new wave of biotech startups is redefining the industry by combining scientific innovation with sustainability and social responsibility.

Emerging players are focusing on:

Reducing reliance on antibiotics in plasmid production

Engineering high-yield, efficient cell lines

Developing biodegradable bioprocess materials

Innovation ecosystems supported by incubators, accelerators, and academic partnerships are fostering collaboration across disciplines. Open-science initiatives and consortia are helping address shared challenges such as cost, scalability, and environmental impact.

Vector Type Insights

Adeno-Associated Virus (AAV) currently dominates the market due to its strong safety profile and versatility across gene therapy applications. Its success is reinforced by multiple approved therapies and expanding clinical adoption.

Lentiviral vectors, however, are projected to grow at the fastest rate. Their ability to carry larger genetic payloads and function in both dividing and non-dividing cells makes them essential for advanced therapies such as CAR-T cell treatments. Their capacity for long-term gene expression further enhances their clinical and commercial value.

Workflow Insights

Downstream Processing (Dominant Segment – 54%)

Downstream processing remains the backbone of manufacturing, ensuring product purity, safety, and regulatory compliance. It includes critical steps such as purification, filtration, and formulation.

Technologies driving this segment include:

Chromatography systems

Ultrafiltration and tangential flow filtration

Membrane-based purification techniques

Its dominance stems from its essential role in removing impurities such as host cell proteins, endotoxins, and residual DNA.

Upstream Processing (Fastest Growing)

Upstream processing is witnessing rapid growth due to advancements in:

Cell line engineering

High-density bioreactors

Suspension-based culture systems

Automation and AI-driven optimization are enabling better control, higher yields, and reduced development timelines, positioning upstream processes as a key driver of future efficiency.

Application Insights

Vaccinology held the largest market share, driven by the rapid development and deployment of vector-based vaccines during the COVID-19 pandemic.

Cell therapy is the fastest-growing segment, offering transformative potential in treating cancer and genetic diseases through targeted gene delivery.

End-User Insights

Research institutes dominate early-stage development, contributing foundational discoveries and innovations.

Pharmaceutical and biotech companies are the fastest-growing segment, driven by significant capital investment and faster commercialization cycles.

Disease Insights

Cancer represents the largest and fastest-growing application area, driven by increasing research into gene-based oncology therapies. Additionally, rare and genetic disorders remain a major focus due to the high unmet medical need, with over 350 million people affected globally.

Regional Insights

North America

North America leads the global market due to strong research infrastructure, significant funding, and a high concentration of biotech companies. The region also accounts for the majority of global gene therapy clinical trials.

Asia-Pacific

Asia-Pacific is the fastest-growing region, driven by:

Increasing healthcare investments

Expanding biotech ecosystems

Government support for innovation

Countries such as China, India, Japan, and South Korea are rapidly enhancing their manufacturing capabilities and clinical research output.

Europe

Europe remains a key hub, supported by strong regulatory frameworks and investments in advanced therapy medicinal products (ATMPs). Collaboration between academia and industry continues to drive innovation and commercialization.

Middle East & Africa

This region is emerging gradually, with investments in biotechnology infrastructure and growing interest in precision medicine. However, challenges such as limited skilled workforce and infrastructure remain.

Latin America

Latin America is gaining momentum through increased participation in clinical trials and government-backed initiatives. Brazil and Mexico are leading regional growth, supported by expanding biotech capabilities.

Viral Vectors & Plasmid DNA Manufacturing Market Companies

- Novasep

- Aldevron

- Creative Biogene

- The Cell and Gene Therapy Catapult

- Cobra Biologics

Market Segmentation

By Vector Type

- Adenovirus

- Plasmid DNA

- Lentivirus

- Retrovirus

- AAV

- Others

By Application

- Gene Therapy

- Antisense &RNAi

- Cell Therapy

- Vaccinology

By Workflow

- Upstream Processing

- Vector Recovery/Harvesting

- Vector Amplification & Expansion

- Downstream Processing

- Fill-finish

- Purification

By End-User

- Biopharmaceutical and Pharmaceutical Companies

- Research Institutes

By Disease

- Genetic Disorders

- Cancer

- Infectious Diseases

- Others

By Geography

- North America

- U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of the World

Get Sample Link: https://www.precedenceresearch.com/sample/1012

Also Read :https://www.marketstatsinsight.com/generic-sterile-injectable-market/

- Corporate Wellness Market Surges Toward USD 500.09 Billion by 2035 - April 22, 2026

- Portable Medical Devices Market Surges Toward USD 221.71 Billion by 2035 - April 22, 2026

- Infant Incubator Market Set to Surpass USD 3.27 Billion by 2035 - April 22, 2026